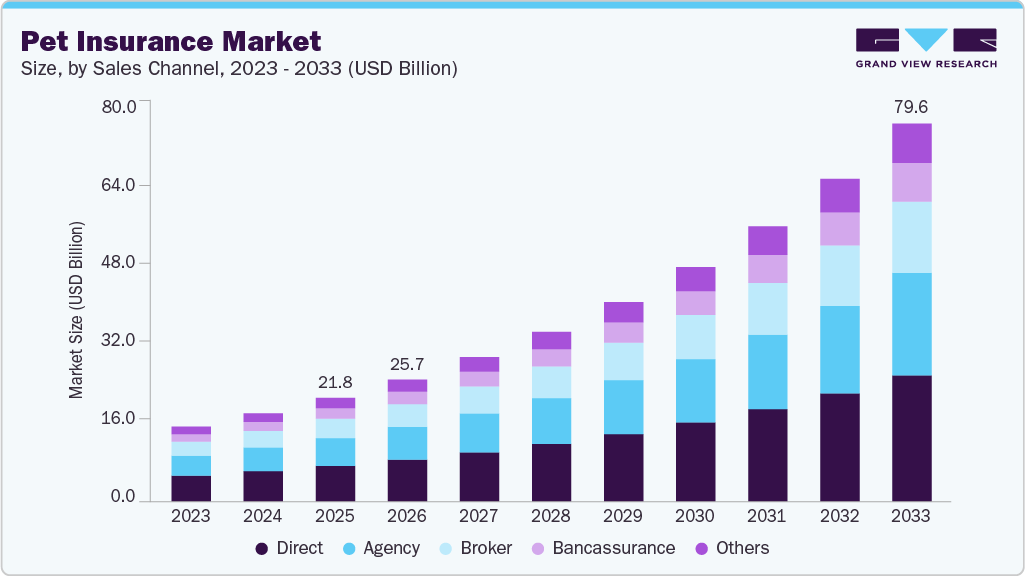

Pet Insurance Market growing at a CAGR of 17.53% from 2026 to 2033

The global pet insurance market size was estimated at USD 21.84 billion in 2025 and is projected to reach USD 79.61 billion by 2033, growing at a CAGR of 17.53% from 2026 to 2033. The growing pet population, the adoption of insurance in underpenetrated markets, increasing veterinary care costs, initiatives by key companies, rising penetration of Insurtech, and humanization of pets are some of the critical drivers of this market.

Key Market Trends & Insights

- The Europe pet insurance market held the largest share of 41.23% of the global market in 2025.

- By coverage, the accident & illness segment held the largest share of 85.17% in 2025.

- By animal, the dogs segment dominated the global pet insurance market in 2025.

- Based on sales channel, the others segment is expected to grow at the fastest rate over the forecast period.

Market Size & Forecast

- 2025 Market Size: USD 21.84 Billion

- 2033 Projected Market Size: USD 79.61 Billion

- CAGR (2026-2033): 17.53%

- Europe: Largest market in 2025

- Asia Pacific: Fastest-growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/pet-insurance-market/request/rs1

According to the most recent data from NAPHIA’s 2024 State of the Industry (SOI) report, 6.25 million pets are insured in North America at the moment. Compared to 2022, when there were 5.36 million pets insured in the region, this indicates a 16.6% growth. The market for pet insurance is anticipated to grow as a result of the rising prevalence of diseases in dogs and cats, as well as the growing trend of pet adoption. The industry is growing because insurance has emerged as a vital tool for pet owners to manage the costs of serious medical conditions like cancer, chronic illnesses, and unintentional injuries. Since treatments often require substantial capital investments, specialized staff, and cutting-edge diagnostic technology, which increases costs for pet owners, the rise in demand for veterinary healthcare facilities further encourages adoption.

The rise in pet adoption, particularly during the COVID-19 pandemic, played a catalytic role in reshaping the market. A survey by Petplan in the UK revealed that nearly 26% of owners welcomed a new pet during lockdowns, with companionship and work-from-home flexibility cited as major reasons. This surge in pet ownership translated into stronger demand for financial protection, with about one-fifth of new owners considering insurance policies. Companies like Animal Friends Insurance have also innovated by offering coverage for remote veterinary consultations, reflecting the trend of digital healthcare integration in the pet sector.

The sector is also being shaped by new trends that are specific to each country. The majority of insurance claims in Australia are for “designer dogs,” according to data from April 2025. This suggests that there is an increasing need for plans that cover health risks specific to certain breeds and genetics. According to data from June 2025, the total number of pet owners in South Korea rose to over 15 million, indicating a sizable untapped insurance market. Long-term market potential is further stimulated by expanding urbanization and pet humanization. Another changing aspect is regulatory scrutiny. The Australian Securities and Investments Commission (ASIC), aiming to investigate consumer protection and compliance practices, temporarily halted pet insurance plans from well-known companies, such as Medibank and Woolworths, in 2023. These instances highlight the importance of transparent product design and a reasonable price in maintaining consumer trust.

Furthermore, a crucial trend in the sector is the inclusion of pet insurance in employee benefits. Employers are including pet insurance benefits in their employee health insurance packages with the aim of retaining Gen Z and millennial employees. This illustrates how pet care is becoming more deeply rooted in the corporate and consumer ecosystems.

Overall, with rising pet ownership, higher veterinary costs, growing pet humanization, and innovations in policy design, the global pet insurance market is poised for robust growth. However, evolving regulatory oversight and shifting consumer expectations will remain critical determinants of how insurers design sustainable and consumer-friendly offerings.

In addition, Insurtechs are reshaping the industry by introducing AI-driven underwriting, digital claims management, and telehealth integration, which streamline processes and improve customer experience. Entry of these platforms into the sector highlights global momentum, with technology-driven platforms enabling faster product launches and tailored plan coverage. Automation and big data analytics are allowing insurers to assess risk more accurately, reduce fraud, and improve pricing structures. Insurtechs also leverage mobile-first distribution channels, expanding accessibility and engagement with younger, digital-native pet owners. Besides, partnerships with veterinary networks and embedded insurance models are making policies more relevant and easier to purchase. Overall, insurtech is driving efficiency, affordability, and personalization, accelerating the adoption of pet insurance worldwide.

Market Concentration & Characteristics

The pet insurance industry is experiencing a high degree of innovation, driven not only by advanced veterinary medicine and diversified coverage plans, but also by the growing role of insurtech. Chinese InsurTech players and global digital-first insurers are entering the market, with the help of technologies such as AI, big data, and digital platforms to streamline underwriting, personalize coverage, and enhance claims management. These technologies improve customer experience, reduce fraud, and enable real-time policy adjustments. Rising pet adoption and humanization trends further amplify demand, while the expansion of treatment options and increasing veterinary costs make tech-enabled insurance solutions increasingly attractive.

Expansion in the market is marked by both geographic reach and broadening of coverage offerings. Apart from business expansion strategies, such as Trupanion’s 2024 launch in Switzerland and Germany, domestic insurers are also diversifying their portfolios. Universal Sompo, for instance, is an Indian insurance company that has recently expanded into pet insurance. This reflects a rise in awareness of pet healthcare and also demand for financial security. Such initiatives highlight how insurers are tailoring products to local markets while tapping into global trends of increasing pet ownership and the growing need for affordable veterinary care.

Pet Insurance Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2026 |

USD 25.70 billion |

|

Revenue forecast in 2033 |

USD 79.61 billion |

|

Growth rate |

CAGR of 17.53% from 2026 to 2033 |

|

Historical Period |

2021 – 2024 |

|

Actual data |

2025 |

|

Forecast period |

2026 – 2033 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2026 to 2033 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments Covered |

Coverage, animal, sales channel, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East and Africa |

|

Country scope |

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Denmark; Sweden; Norway; Austria; Hungary; Poland; Romania; Czech Republic; Switzerland; Luxembourg; Portugal; Belgium; Japan; China; India; South Korea; Australia; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait; Qatar; Oman |

|

Key companies profiled |

Trupanion, Inc.; Deutsche Familienversicherung AG (DFV); Petplan (Allianz); Jab Holding Company; Direct Line; EQT Group; Lassie; Getsafe GmbH; Waggel Limited; Feather Insurance; Napo Limited; Tesco; Sainsbury Bank Plc; Fressnapf Holding SE; MetLife Services and Solutions, LLC; HDFC Ergo; Nationwide Mutual Insurance Company; Anicom Insurance; AliPay |

|

Customization scope |

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |