Global Positioning Systems Market Size, Share & Trends Analysis growing at a CAGR of 16.1% from 2023 to 2030

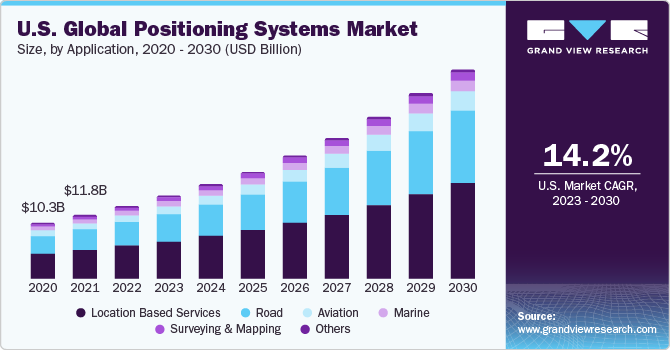

The global positioning systems market size was estimated at USD 94.25 billion in 2022 and is projected to reach USD 311.82 billion by 2030, growing at a CAGR of 16.1% from 2023 to 2030. The increasing penetration of smartphones and the proliferation of GPS-enabled vehicles are projected to bolster the market’s growth during the forecast period.

Key Market Trends & Insights

- Asia Pacific is leading the market, with a market share of 36.1% in 2022.

- North America is one of the regions witnessing significant growth in the market.

- Based on deployment, the consumer devices segment accounted for the highest revenue share of 45.2% in 2022.

- Based on application, the location-based services segment represented the leading share of 42.9% of the global positioning systems market in 2022.

Market Size & Forecast

- 2022 Market Size: USD 94.25 Billion

- 2030 Projected Market Size: USD 311.82 Billion

- CAGR (2023-2030): 16.1%

- Asia Pacific: Largest market in 2022

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/gps-market/request/rs1

Moreover, the surging use of social media across developing countries and growth in mergers and acquisitions between component manufacturers and integrators are poised to stoke the growth of the global positioning systems market.

Over the years, the global positioning system has become a common tool used for navigation. The past couple of years have witnessed a rise in the use of GPS-enabled smartphones. The growing adoption of e-hailing services across the globe is further likely to escalate the demand for GPS-enabled smartphones. The system used in road applications provides various benefits to customers, including ease of traveling and accurate monitoring of operations and assets. Increasing smart mobility applications, such as navigation, fleet management, satellite road traffic monitoring, and several others, are expected to propel the market over the forecast period.

Prominent GPS component manufacturers such as Qualcomm Inc., Hexagon AB, Broadcom Inc., Trimble Navigation Limited, MiTAC Digital Technology Corporation (Navman), TomTom N.V, Rockwell Collins Inc., Texas Instruments Inc., Garmin Ltd., and Mio Technology Corporation are estimated to make significant investments in R&D activities. The strategy is anticipated to help them develop new innovative deployments, solutions, and augmented services, which will strengthen their position in the global arena.

Besides, mergers and acquisitions between component manufacturers and system integrators are expected to help GPS market players capture a high revenue share and increase overall profitability over the coming years. For instance, in March 2023, Topcon Positioning Systems acquired Digital Construction Works (DCW. With this acquisition, Topcon aims to leverage DCW’s expertise in providing a platform that enables customers to effectively manage and optimize construction data across various applications and software. DCW’s services and software integration platform will assist customers in efficiently navigating and maximizing the utilization of construction data, enhancing productivity, and streamlining workflows in the construction industry.