Solid-State Battery Materials Market growing at a CAGR of 30.3% from 2025 to 2033

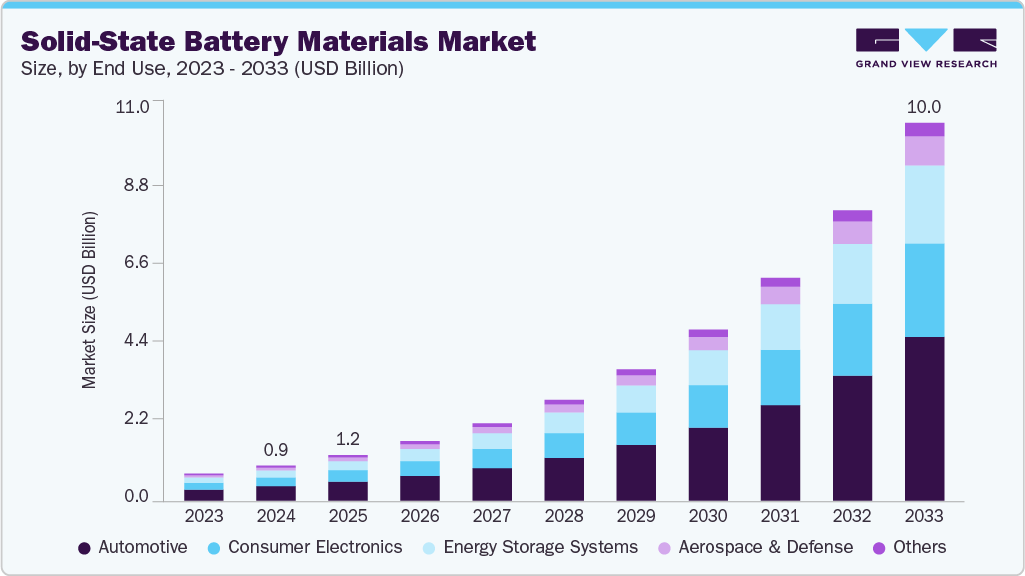

The global solid-state battery materials market size was estimated at USD 0.93 billion in 2024 and is projected to reach USD 10.04 billion by 2033, growing at a CAGR of 30.3% from 2025 to 2033. The growth is driven by the rising demand for safer and higher energy density energy storage solutions across various industries. Solid-state batteries, which replace liquid electrolytes with solid materials, offer enhanced safety by eliminating risks associated with leakage and combustion.

Key Market Trends & Insights

- North America dominated the solid-state battery materials market with the largest revenue share of 32.2% in 2024.

- By battery type, sodium-based solid-state batteries segment is expected to grow at the fastest CAGR of 30.8% from 2025 to 2033 in terms of revenue.

- By end use, automotive segment is expected to grow at the fastest CAGR of 30.9% from 2025 to 2033 in terms of revenue.

Market Size & Forecast

- 2024 Market Size: USD 0.93 Million

- 2033 Projected Market Size: USD 10.04 Million

- CAGR (2025-2033): 30.3%

- Asia Pacific: Largest market in 2024

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/solid-state-battery-materials-market-report/request/rs1

The increasing adoption of electric vehicles (EVs) has significantly accelerated the need for advanced battery technologies that provide longer driving ranges, faster charging, and greater reliability. This transition is compelling manufacturers to invest heavily in solid-state materials such as ceramics, sulfides, and polymers to enhance battery performance and lifespan.

Technological advancements in battery chemistry and materials science are further propelling the growth of the solid-state battery materials market. Research initiatives focused on improving ionic conductivity and reducing interfacial resistance are enabling the development of more efficient and commercially viable solid-state batteries. Companies and research institutions are collaborating to innovate new material compositions that can achieve higher energy densities while maintaining stability and scalability. Such innovations are not only improving the performance of next-generation batteries but also reducing production costs, making solid-state technologies more accessible to a wider range of applications.

The growing emphasis on sustainability and environmental conservation is another key driver of the market. Solid-state batteries utilize materials that are less hazardous and more recyclable compared to conventional lithium-ion batteries, aligning with global goals for cleaner energy storage solutions. Governments and regulatory bodies across regions are promoting eco-friendly technologies through incentives and funding programs, encouraging industries to adopt greener alternatives. As a result, material manufacturers are increasingly focusing on developing solid-state components that reduce carbon emissions and enhance the recyclability of battery systems.

Market Concentration & Characteristics

The global solid-state battery materials market exhibits a moderate to high degree of innovation, characterized by continuous advancements in electrolyte materials, interface engineering, and manufacturing techniques. Companies and research institutions are investing heavily in R&D to enhance ionic conductivity, energy density, and overall battery stability, driving rapid technological evolution. The market has also witnessed strategic mergers, acquisitions, and collaborations among leading players and startups, aimed at accelerating commercialization and scaling production capabilities. These consolidations are helping firms strengthen their intellectual property portfolios and reduce the time-to-market for innovative solid-state solutions, thereby intensifying competition among key participants.

Regulatory frameworks and environmental policies have a significant influence on market dynamics, particularly in promoting sustainable and safe battery materials. Stringent government regulations on emissions and safety standards are encouraging the adoption of eco-friendly materials and manufacturing processes. The availability of service substitutes remains limited, as solid-state batteries offer distinct advantages in safety and performance compared to conventional lithium-ion technologies. However, ongoing R&D in hybrid and semi-solid batteries presents potential competitive alternatives. End user concentration is notably high in sectors such as electric vehicles, consumer electronics, and renewable energy storage, where the demand for compact, efficient, and durable energy solutions is driving large-scale adoption and sustained investment in solid-state battery materials.

End Use Insights

The automotive segment dominated the global solid-state battery materials market, accounting for a revenue share of 41.4% in 2024, driven by the rising adoption of electric vehicles (EVs) and the demand for safer, higher-capacity energy storage systems. Automakers are increasingly investing in solid-state technology to enhance vehicle range, reduce charging time, and improve battery lifecycle. Stringent emission regulations across major economies are accelerating the transition from conventional lithium-ion to solid-state batteries. Furthermore, collaborations between battery manufacturers and automotive OEMs are expediting large-scale commercialization. The focus on lightweight, compact, and thermally stable materials further strengthens market expansion in this segment.

Energy & power segment is expected to grow significantly at CAGR of 30.5% over the forecast period, driven by growing investments in renewable energy infrastructure and grid storage systems requiring reliable, high-energy-density batteries. Solid-state batteries provide longer operational life, enhanced safety, and better thermal stability compared to traditional systems, making them ideal for energy storage applications. Increasing global energy consumption and the need for sustainable power management solutions are fueling adoption. Additionally, the declining cost of advanced solid electrolytes is improving scalability for large-scale installations. Government initiatives promoting smart grids and clean energy further contribute to segment growth.

Battery Type Insights

Lithium-based solid-state batteries segment dominated the global solid-state battery materials market, accounting for a revenue share of 82.5% in 2024, driven by technological advancements in solid electrolytes, particularly sulfide and oxide-based materials that enhance ionic conductivity and battery performance. These batteries are gaining traction due to their higher energy density and superior safety compared to liquid lithium-ion systems. Growing R&D investments from companies like Toyota, Solid Power are accelerating innovation. The rapid expansion of EV and consumer electronics markets is also increasing demand for efficient lithium-based solid-state materials. Moreover, manufacturing process optimization and cost reduction efforts are improving commercialization potential.

Sodium-based solid-state batteries segment is anticipated to grow at the fastest CAGR of 30.8% during the forecast period, driven by need for cost-effective and resource-abundant alternatives to lithium-based systems. Sodium’s widespread availability and lower material cost make it attractive for large-scale energy storage and grid applications. Research advancements in solid electrolytes and sodium anode materials are enhancing performance and stability. These batteries offer strong potential for regions with limited lithium resources, supporting energy independence and sustainability. In addition, industrial and government-backed projects are focusing on sodium solid-state technologies to diversify the global energy storage landscape.

Solid-State Battery Materials Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2025 |

USD 1.21 billion |

|

Revenue forecast in 2033 |

USD 10.04 billion |

|

Growth rate |

CAGR of 30.3% from 2025 to 2033 |

|

Base year for estimation |

2024 |

|

Historical data |

2021 – 2023 |

|

Forecast period |

2025 – 2033 |

|

Quantitative units |

Revenue in USD million/billion, and CAGR from 2025 to 2033 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

End use, battery type, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

|

Country scope |

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; India; China; Japan; South Korea |

|

Key companies profiled |

QuantumScape Corporation; Toyota Motor Corporation; Solid Power, Inc.; Samsung SDI Co. Ltd.; LG Energy Solution Ltd.; Ilika plc; Murata Manufacturing Co., Ltd.; Hitachi Zosen Corporation; Panasonic Holdings Corporation |

|

Customization scope |

Free report customization (equivalent to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |