Solid Oxide Fuel Cell Market growing at a CAGR of 15.7% from 2025 to 2033

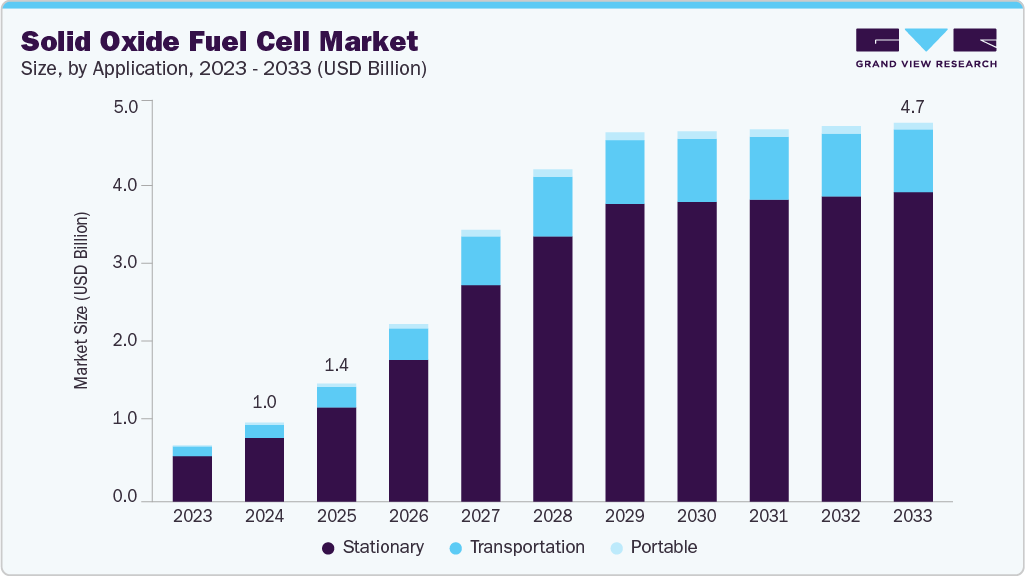

The global solid oxide fuel cell market size was estimated at USD 1.0 billion in 2024 and is anticipated to reach USD 4.7 billion by 2033, growing at a CAGR of 15.7% from 2025 to 2033. Rising demand for clean and efficient energy generation systems, especially in decentralized and off-grid applications, is a key factor driving the adoption of SOFC technology.

Key Market Trends & Insights

- North America solid oxide fuel cell market held the largest share of 34.52% of the global market in 2024.

- The solid oxide fuel cell industry in the U.S. is expected to grow significantly over the forecast period.

- By application, the stationary segment held the highest market share of 80.13% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 1.0 Billion

- 2033 Projected Market Size: USD 4.7 Billion

- CAGR (2025-2033): 15.7%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/solid-oxide-fuel-cells-market/request/rs1

Solid oxide fuel cells offer high fuel-to-electricity conversion efficiency, low emissions, and fuel flexibility, making them increasingly attractive in sectors ranging from industrial and commercial power generation to auxiliary power units for transportation. In recent years, heightened concerns about energy security and decarbonization have accelerated the deployment of Solid oxide fuel cells (SOFC) systems in both stationary and mobile energy infrastructures, particularly in countries advancing toward net-zero goals. The SOFC market benefits from ongoing federal investments in hydrogen infrastructure and resilient grid technologies in the United States.

Several pilot projects have demonstrated the role of SOFCs in enhancing microgrid reliability and lowering carbon intensity in commercial buildings. The country’s growing shift from centralized fossil-fuel-based systems to localized clean energy alternatives is expected to stimulate demand for SOFC installations further. In addition, supportive policy frameworks, increasing private sector collaboration, and strategic partnerships with energy utilities enhance the scalability of SOFC deployments in urban and industrial zones. These trends point toward long-term adoption across the distribution of energy and backup power applications.

Japan continues to lead the global SOFC market, owing to its strong focus on hydrogen utilization and energy efficiency. The country has heavily invested in residential fuel cell systems like ENE-FARM. It is actively scaling up its hydrogen supply chain infrastructure to support the broader adoption of fuel cell technologies. SOFCs are increasingly being integrated into smart home systems and combined heat and power (CHP) units, contributing to widespread use. With national targets to become carbon-neutral by 2050 and ongoing R&D efforts aimed at cost reduction and performance optimization, Japan will likely maintain a dominant position in the global SOFC landscape during the forecast period.

Solid oxide fuel cells provide a sustainable and highly efficient power solution with minimal environmental impact. Their versatility in using various fuels such as hydrogen, biogas, and natural gas adds to their appeal in an evolving energy ecosystem. As grid stability, resilience, and emissions reduction become top priorities globally, SOFC technology is emerging as a cornerstone of next-generation energy systems, offering robust performance in centralized utilities and localized, self-sustained networks.

Drivers, Opportunities & Restraints

The global market for solid oxide fuel cell (SOFC) is primarily driven by the increasing demand for high-efficiency, low-emission energy systems across industrial, commercial, and residential sectors. The growing need to decarbonize power generation, improve energy reliability, and transition toward cleaner fuels, particularly hydrogen, has placed SOFC technology at the forefront of sustainable energy solutions.

Governments worldwide support fuel cell R&D through public-private partnerships, subsidies, and clean energy mandates, enhancing the market outlook. Additionally, SOFCs offer fuel flexibility and quiet, modular operation, making them ideal for backup power, combined heat and power (CHP) applications, and off-grid energy generation in high-demand sectors such as data centers and healthcare.

Opportunities within the SOFC market are expanding rapidly, particularly with the global pivot toward hydrogen economies. Advancements in material science and system integration are driving down costs and improving thermal efficiency, making SOFC systems more commercially viable. Emerging applications in distributed power systems, marine propulsion, and auxiliary power units for electric vehicles offer new avenues for growth.

Furthermore, increasing investments in green hydrogen infrastructure and electrolyzer integration highlight SOFCs’ potential in reversible energy systems. However, several restraints continue to affect large-scale adoption. High upfront capital costs, long start-up times, and technical complexity in system maintenance remain significant challenges. Limited hydrogen distribution networks, regulatory uncertainty, and slow commercialization timelines constrain market expansion, especially in developing regions.

Application Insights

Stationary segment held the revenue share of over 80.13% in 2024. The stationary segment held the largest revenue share of approximately 80.13% in 2024. This dominance is attributed to the growing deployment of SOFC systems in stationary power generation across commercial buildings, data centers, hospitals, and utility-scale energy projects. These systems are increasingly favored for their high efficiency, fuel flexibility, and ability to provide continuous, low-emission electricity and heat. As demand for decentralized energy solutions rises, stationary SOFCs are being adopted for combined heat and power (CHP) applications, especially in regions with aging grid infrastructure or stringent emission regulations.

The adoption of stationary SOFCs is further driven by industries and institutions prioritizing energy resilience, cost savings, and carbon reduction. For instance, many corporate campuses and critical facilities are investing in SOFC-powered microgrids to ensure uninterrupted power during outages while reducing reliance on diesel generators. Additionally, their compatibility with hydrogen and biogas makes stationary SOFCs a strategic fit for net-zero and low-carbon energy transition goals. As urban power loads grow due to increasing electrification, digitalization, and climate adaptation needs, the stationary segment will remain the cornerstone of SOFC market growth over the forecast period.

Solid Oxide Fuel Cell Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2025 |

USD 1.4 billion |

|

Revenue forecast in 2033 |

USD 4.7 billion |

|

Growth rate |

CAGR of 15.7% from 2025 to 2033 |

|

Base year for estimation |

2024 |

|

Historical data |

2021 – 2023 |

|

Forecast period |

2025 – 2033 |

|

Quantitative Units |

Revenue in USD million/billion, volume in units, capacity in kW, and CAGR from 2025 to 2033 |

|

Report coverage |

Revenue forecast, volume forecast, capacity forecast, competitive landscape, growth factors, and trends |

|

Segments covered |

Application, region |

|

Regional scope |

North America; Europe; Asia Pacific; Rest of World |

|

Country scope |

U.S.; Germany; UK; France; China; Japan; South Korea |

|

Key companies profiled |

Bloom Energy; Mitsubishi Power Ltd.; Ceres; General Electric; FuelCell Energy Inc.; Ningbo SOFCMAN Energy; KYOCERA Corporation; AVL; NGK SPARK PLUG CO., LTD. |

|

Customization scope |

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |