Semiconductor Fabless Market Size, Share & Trends Analysis growing at a CAGR of 9.9% from 2024 to 2030

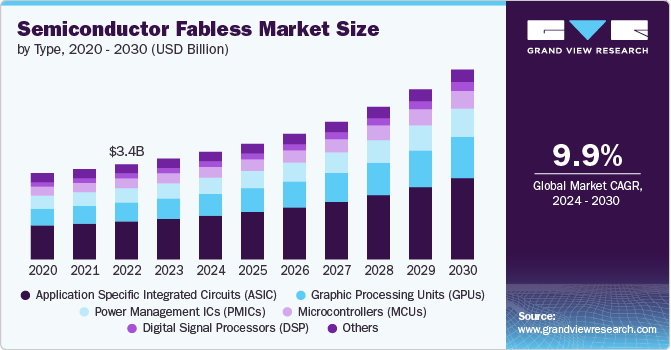

The global semiconductor fabless market size was estimated at USD 3.56 billion in 2023 and is projected to reach USD 6.71 billion by 2030, growing at a CAGR of 9.9% from 2024 to 2030. The market’s growth can be attributed to the increasing demand for advanced semiconductor devices, particularly in sectors such as consumer electronics, healthcare, and automotive electronics.

Key Market Trends & Insights

- The Asia Pacific semiconductor fabless market accounted for a 56.05% share of the global market in 2023.

- The U.S. semiconductor fabless market is expected to grow at a significant CAGR over the forecast period.

- Based on type, the application specific integrated circuits (ASIC) segment dominated the market in 2023.

- Based on end-use, the consumer electronics segment dominated the market in 2023.

Market Size & Forecast

- 2023 Market Size: USD 3.56 Billion

- 2030 Projected Market Size: USD 6.71 Billion

- CAGR (2024-2030): 11.7%

- Asia Pacific: Largest market in 2023

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/semiconductor-fabless-market-report/request/rs1

Technological advancements in semiconductor fabrication processes also play a pivotal role in the market’s growth. In addition, the rise of digital transformation across various industries is accelerating the demand for semiconductor components, thereby driving the market’s growth.

The rapid advancement of artificial intelligence (AI) and machine learning (ML) technologies is driving the growth of the market. As AI and ML applications become increasingly prevalent across industries such as automotive, healthcare, and consumer electronics, the demand for specialized semiconductor solutions that can handle complex computations and large data sets is growing. Semiconductor fabless companies focus on designing innovative chips without the need for manufacturing facilities. They are focusing on this trend by developing advanced processors and accelerators tailored for AI and ML workloads. This focus on high-performance and energy-efficient chips supports the growing ecosystem of AI-driven applications and helps market companies gain a competitive edge in the market.