Industrial Wax Market growing at a CAGR of 4.9% from 2026 to 2033

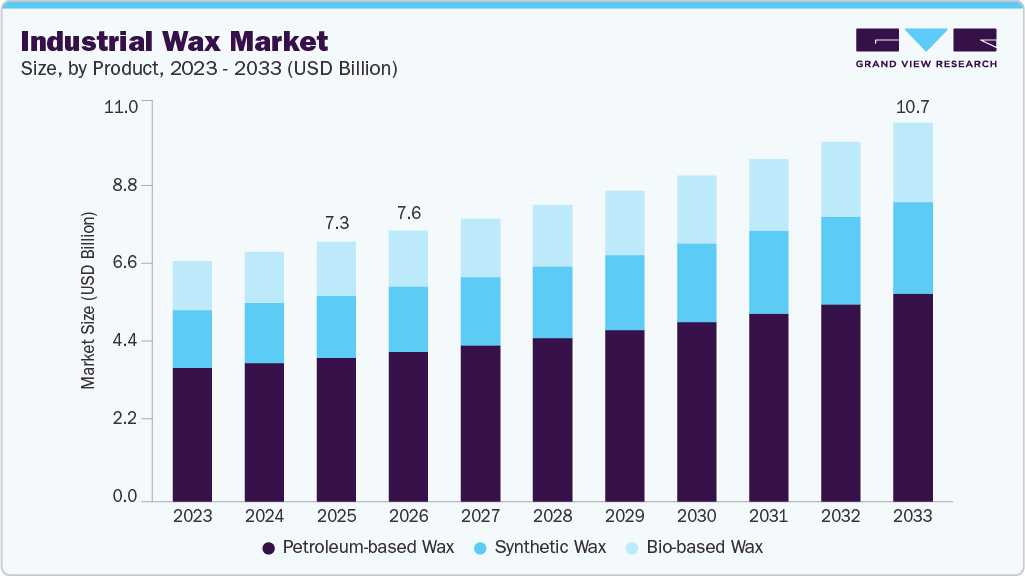

The global industrial wax market size was estimated at USD 7.33 billion in 2025 and is projected to reach USD 10.69 by 2033, growing at a CAGR of 4.9% from 2026 to 2033. The market growth is primarily driven by steady demand from candles, packaging, plastics & rubber processing, and adhesives, where waxes are critical for coating, lubrication, dispersion, and moisture-barrier functions.

Key Market Trends & Insights

- Asia Pacific dominated the industrial wax market with the largest revenue share of 43.0% in 2025.

- China’s industrial wax market accounted for a 46.3% share of Asia Pacific in 2025.

- By product, the petroleum-based wax segment held the largest revenue share of 55.4% in 2025 in terms of value.

- By application, the candles segment held the largest revenue share of 33.5% in 2025 in terms of value.

Market Size & Forecast

- 2025 Market Size: USD 7.33 billion

- 2033 Projected Market Size: USD 10.69 billion

- CAGR (2026-2033): 4.9%

- Asia Pacific: Largest market in 2025

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/industrial-wax-market-report/request/rs1

Growth in consumer goods, flexible packaging, and hygiene products, particularly in Asia Pacific and North America, continues to support volume consumption of petroleum-based waxes. In parallel, industrial expansion and polymer processing activities are driving demand for synthetic waxes due to their superior thermal stability and consistent performance. The rising consumption of cosmetics, toiletries, and pharmaceutical formulations is driving value growth, benefiting both high-purity mineral waxes and specialty synthetic alternatives offered by integrated players such as ExxonMobil, Shell, BASF, Dow, and Evonik.

The industrial wax industry presents significant opportunities driven by the structural shift toward bio-based and specialty waxes, supported by sustainability mandates, decarbonization goals, and tightening environmental regulations across Europe and North America. Bio-based waxes derived from vegetable and renewable feedstocks are gaining traction in cosmetics, packaging, and pharmaceutical applications, creating premium growth avenues for chemical innovators and specialty producers. Moreover, advancements in synthetic wax formulations, enabling improved performance in hot-melt adhesives, plastics processing, and high-temperature applications, are expanding addressable markets beyond traditional uses. Emerging economies, particularly in Asia Pacific and Latin America, offer long-term volume growth potential driven by rising manufacturing output, urbanization, and increased consumption of candles, packaging materials, and personal care products.

Despite stable demand fundamentals, the industrial wax market faces challenges related to feedstock price volatility, supply chain disruptions, and environmental scrutiny, particularly for petroleum-based waxes. Fluctuations in crude oil refining economics directly affect the availability and pricing of mineral waxes, putting downstream manufacturers under margin pressure. In addition, stringent environmental regulations and sustainability expectations are accelerating the transition away from fossil-based waxes, increasing compliance costs for traditional producers. Bio-based waxes, while attractive, face challenges related to higher production costs, limited scale, and feedstock availability, which can restrict widespread adoption. Furthermore, intense competition among global integrated oil & gas companies and specialty chemical manufacturers continues to exert pressure on pricing, differentiation, and long-term profitability.

Market Concentration & Characteristics

The industrial wax market is moderately consolidated, with competition shaped by the presence of large integrated oil & gas companies, diversified chemical manufacturers, and specialized wax producers. Major petroleum-based wax supply is dominated by integrated refiners such as Sinopec Corp, China National Petroleum Corporation (CNPC), Exxon Mobil Corporation, BP p.l.c., Royal Dutch Shell p.l.c., Sasol Limited, and HollyFrontier Corporation, which benefit from secure feedstock access, large-scale refining assets, and global distribution networks. These players compete primarily on volume, cost efficiency, and supply reliability, serving high-demand applications such as candles, packaging, and rubber processing, particularly across Asia Pacific and North America.

In contrast, synthetic and specialty wax segments are led by chemical companies including BASF SE, Dow, Evonik Industries AG, Mitsui Chemicals, Honeywell International, Baker Hughes, Nippon Seiro, and The International Group (IGI), where differentiation is driven by product performance, purity, and application-specific formulations. These players focus on value-added applications such as adhesives, plastics processing, cosmetics, and pharmaceuticals, where margins are higher, and customer qualification cycles are longer. Competitive intensity is increasing as companies expand bio-based wax portfolios, invest in R&D, and pursue strategic partnerships and capacity expansions to address sustainability requirements and evolving end-user specifications, making innovation and application expertise key determinants of long-term market positioning.

Product Insights

The petroleum-based wax segment dominated the global industrial wax market in 2025, accounting for the largest revenue share of approximately 55.4%, driven by its cost competitiveness, large-scale availability, and broad applicability across high-volume end uses. Petroleum-based waxes, including paraffin and microcrystalline waxes, benefit from well-established refining infrastructure and integrated supply chains, particularly among major oil & gas companies. These waxes remain the preferred choice for candles, packaging coatings, rubber processing, and fire logs, where performance requirements are standardized, and price sensitivity remains high. Additionally, consistent demand from emerging economies, coupled with the ability of refiners to supply large volumes reliably, has reinforced the segment’s dominant position in the global market.

In contrast, synthetic and bio-based waxes are gaining traction as higher-growth segments, supported by evolving application requirements and sustainability considerations. Synthetic waxes are increasingly adopted in plastics and rubber processing, hot-melt adhesives, and specialty industrial applications due to their superior thermal stability, controlled molecular structure, and consistent performance, enabling manufacturers to achieve tighter process tolerances. Meanwhile, bio-based waxes, derived from renewable feedstocks, are witnessing accelerating adoption in cosmetics, pharmaceuticals, and sustainable packaging, driven by regulatory pressure, brand-led sustainability initiatives, and consumer preference for bio-based ingredients. Although these segments currently represent a smaller share of total revenue, continued investments in product innovation, capacity expansion, and green chemistry are expected to gradually reshape the product mix over the forecast period.

Industrial Wax Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2026 |

USD 7.64 billion |

|

Revenue forecast in 2033 |

USD 10.69 billion |

|

Growth rate |

CAGR of 4.9% from 2026 to 2033 |

|

Base year for estimation |

2025 |

|

Historical data |

2018 – 2025 |

|

Forecast period |

2026 – 2033 |

|

Quantitative units |

Revenue in USD million/billion, volume in kilotons and CAGR from 2025 to 2033 |

|

Report coverage |

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Product, application, region |

|

Regional scope |

North America; Europe; Asia Pacific; Middle East & Africa; Latin America |

|

Country scope |

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia |

|

Key companies profiled |

Sinopec Corp; China National Petroleum Corporation; HollyFrontier Corporation; Nippon Seiro Co., Ltd; Baker Hughes Company; BP p.l.c.; Exxon Mobil Corporation; Sasol Limited; The International Group, Inc.; Evonik Industries AG; BASF SE; Dow; Honeywell International Inc.; Royal Dutch Shell P.L.C.; Mitsui Chemicals, Inc. |

|

Customization scope |

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |