Building-integrated Photovoltaics Market growing at a CAGR of 21.2% from 2024 to 2030

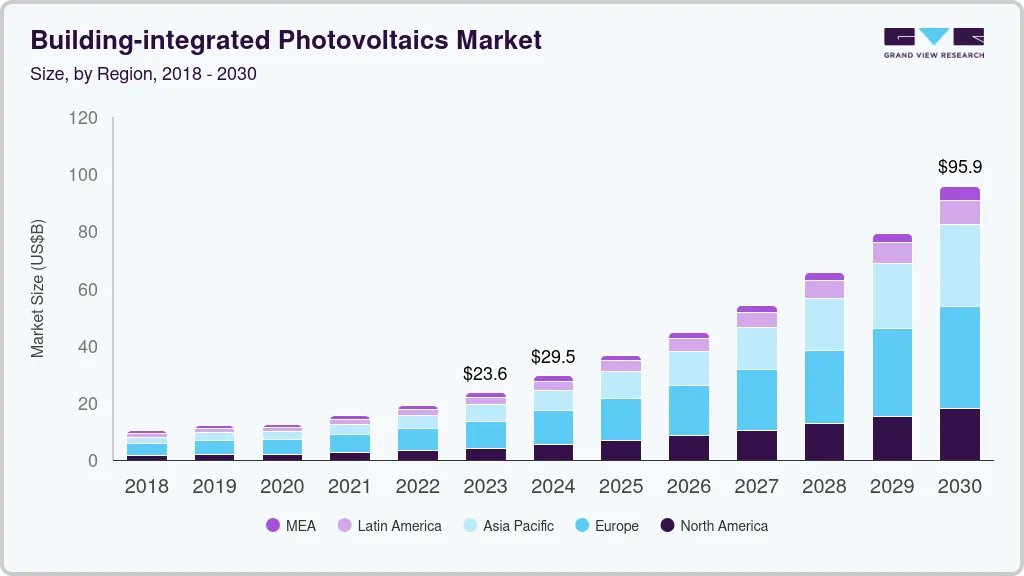

The global building-integrated photovoltaics market size was estimated at USD 23.67 billion in 2023 and is projected to reach USD 89.8 billion by 2030, growing at a CAGR of 21.2% from 2024 to 2030. Rapid expansion of the solar photovoltaic (PV) installation capacities of different countries, coupled with increasing demand for renewable energy sources, is expected to drive the building-integrated photovoltaics (BIPV) market growth across the world.

Key Market Trends & Insights

- Europe dominated the building-integrated photovoltaics market with the largest revenue share of 37.1% in 2023.

- The building-integrated photovoltaics market in U.S. is expected to grow at a significant CAGR of 22.1% from 2024 to 2030.

- The building-integrated photovoltaics market in North America is anticipated to grow at the fastest CAGR over the forecast period.

- Based on application, the roofs segment led the market with the largest revenue share of 66.9% in 2023.

- Based on end use, the residential segment led the market with the largest revenue share of 34.7% in 2023.

Market Size & Forecast

- 2023 Market Size: USD 23.67 Billion

- 2030 Projected Market Size: USD 89.8 Billion

- Europe : Largest market in 2023

- North America: Fastest growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/building-integrated-photovoltaics-bipv-market/request/rs1

Increased awareness for energy security and self-sufficiency and favorable government legislations, coupled with the unilateral obligation of countries such as Germany, Italy, France, the UK, the U.S., China, Japan, and India to the Kyoto Protocol, designated to reduce greenhouse gas (GHG) emissions, are also expected to promote the market growth in the coming years.

The presence of a consumer base with high disposable income levels and the increasing affinity toward integrated installations in residential and commercial buildings in the country are anticipated to boost the demand for the product over the forecast period. In addition, the growing innovation in the domain is projected to increase the operational efficiency of the product, translating into market growth.The market globally is likely to be driven by the growing demand for alternate sources of energy. The demand for building-integrated photovoltaics is likely to be fueled by the high need for integrated roof systems in commercial and industrial establishments. Improvements in the manufacturing technology of thin film BIPV modules and the rising efficiency of the product are expected to drive the market over the forecast period.

The government of France offers the highest FiTs for electricity generated through photovoltaic components, which are essentially integrated into buildings. Capacity generated by photovoltaics integrated into building envelopes accounts for a substantial share of the overall accumulated, installed capacity generated by photovoltaics in the country. The country offers high subsidies and benefits pertaining to the use of building integrated photovoltaics in a bid to encourage such installations in the country.

Market Concentration & Characteristics

The rapid expansion of the solar photovoltaic (PV) installation capacities of different countries, coupled with increasing demand for renewable energy sources, is expected to drive the market growth across the world. Increased awareness for energy security and self-sufficiency and favorable government legislations, coupled with the unilateral obligation of countries such as Germany, Italy, France, the UK, the U.S., China, Japan, and India to the Kyoto Protocol, designated to reduce greenhouse gas (GHG) emissions, are also expected to promote the market growth in the coming years.

Leading players in the market have adopted the strategies like new product launches, mergers & acquisitions and collaborations to maintain their shares in the global market. For instance, in June 2022, Mitrex, a Canadian company that manufactures building integrated photovoltaic systems, unveiled the largest tandem photovoltaic panel, that can generate up to 800W of power in total. The panels have unique anti-reflecting technology and are made of monocrystalline silicon solar cells that optimize the generation of electrical energy.

Technology Insights

Based on technology, the market has been further divided into crystalline silicon, thin film and others. The crystalline silicon segment led the market with the largest revenue share of 70.9% in 2023.Crystalline silicon cells can be integrated into building roofs by using smart mounting systems, which replace the sections of the roof while keeping its integrity intact. This type of integration does not account for large investments and provides high efficiency. Another option of integration is the replacement of roof tiles with crystalline silicon cells. In addition, the market witnesses the use of anti-reflective coatings, which aid the capture of solar energy and provide superior efficiency. Crystalline silicon has the highest energy conversion efficiency at present; commercial modules typically convert 13%-21% of the incident sunlight into electricity.

The thin film segment accounted for the revenue share of 22.2% in 2023 and the market is expected to witness at a sustainable CAGR over the forecast period, due to rapid technological advancements leading to the introduction of advanced products. Thin film BIPVs are readily used in case of considerable weight constraints for the building. In such cases, the building envelope is unable to support the weight of crystalline silicon integration, leading to high demand for thin film integrated installation. Thin film is advantageous as it can be used for curved surfaces owing to its superior flexibility.

Building-integrated Photovoltaics Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2024 |

USD 28.3 billion |

|

Revenue forecast in 2030 |

USD 89.8 billion |

|

Growth rate |

CAGR of 21.2% from 2024 to 2030 |

|

Base year for estimation |

2023 |

|

Historical data |

2018 – 2022 |

|

Forecast period |

2024 – 2030 |

|

Quantitative units |

Revenue in USD million/billion, Volume in Thousand sq. m., Capacity in MW, and CAGR from 2024 to 2030 |

|

Report coverage |

Revenue forecast, Volume forecast, Capacity forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Technology, application, end-use, region |

|

Region scope |

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

|

Country scope |

U.S.; Canada; Mexico; Russia; Poland; Hungary Germany; Netherlands; France; Austria; Switzerland; Belgium; UK; Denmark; Norway; Sweden; Spain; Portugal; Italy; Greece; Croatia China; India; Japan; South Korea; Australia; Malaysia; Singapore; Thailand; Vietnam; Brazil Argentina; Saudi Arabia; UAE; South Africa |

|

Key companies profiled |

SolarWindow Technologies, Inc.; AGC Inc.; Hanergy Mobile Energy Holding Group Limited; The Solaria Corporation; Heliatek GmbH,; Carmanah Technologies Corp. ; Greatcell; Tesla ; BELECTRIC; ertex solartechnik GmbH; Canadian Solar; Onyx Solar Group LLC ; NanoPV Solar Inc. ; SOLAXESS |

|

Customization scope |

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |