Hyperscale Data Center Market growing at a CAGR of 13.6% from 2025 to 2030

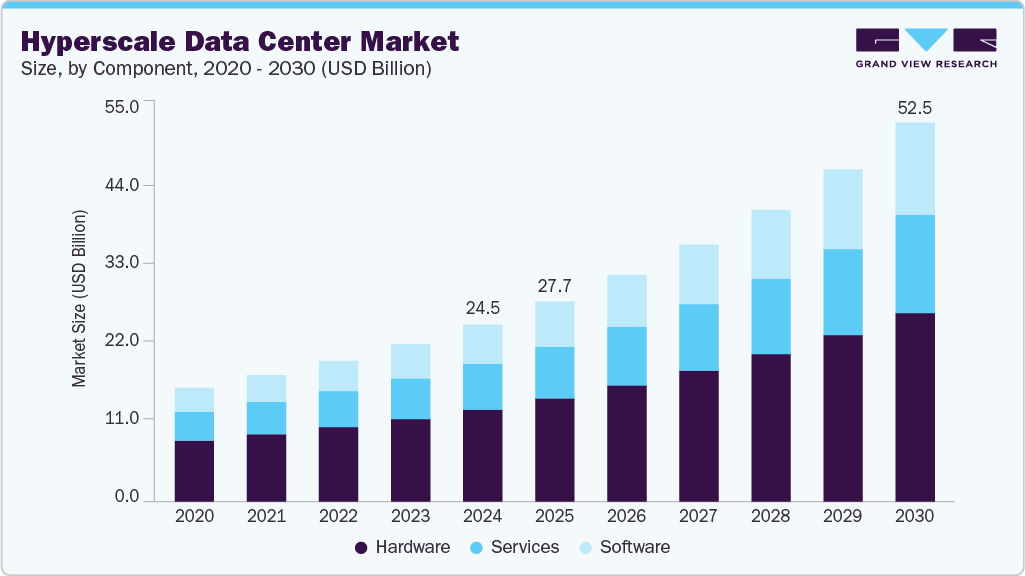

The global hyperscale data center market size was estimated at USD 24.54 billion in 2024 and is projected to reach USD 52.54 billion by 2030, growing at a CAGR of 13.6% from 2025 to 2030, driven by the rapid expansion of cloud computing, artificial intelligence (AI), and big data analytics. As organizations shift from traditional data centers to cloud-based infrastructure, the demand for large-scale, high-performance computing environments has surged.

Key Market Trends & Insights

- North America hyperscale data center market dominated globally with a share of nearly 38.0% in 2024.

- The hyperscale data center market in the U.S. is expected to grow significantly at a CAGR of 13.6% from 2025 to 2030.

- By component, the hardware segment dominated the market with a revenue share of over 50.0% in 2024.

- By power capacity, the 50 MW to 100 MW segment dominated the market with a revenue share of over 33.0% in 2024.

- By enterprise size, the large enterprises segment dominated the market with the largest revenue share of over 73.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 24.54 Billion

- 2030 Projected Market Size: USD 52.54 Billion

- CAGR (2025-2030): 13.6%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/hyperscale-data-center-market/request/rs1

Hyperscale data centers, known for their ability to scale efficiently and support vast volumes of data and computing workloads, are the backbone of cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. These providers continue to invest heavily in building and expanding their global data center footprints to meet escalating user demand and ensure low-latency, high-availability services.

The proliferation of digital services and content consumption also contributes significantly to the hyperscale data center industry. The rise of video streaming, gaming, e-commerce, and social media platforms has created a need for infrastructure that can support massive amounts of data storage and real-time processing. Hyperscale facilities offer the scalability, redundancy, and energy efficiency needed to meet these demands while reducing operational costs per unit of computing. Moreover, the rollout of 5G networks and the growth of Internet of Things (IoT) applications are generating more data at the edge, prompting hyperscale operators to invest in edge data centers and hybrid architectures to process data closer to the source.

Companies across industries are undergoing digital transformation, moving core operations to the cloud to improve agility, scalability, and cost-efficiency. This shift fuels demand for Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and hybrid cloud models, all of which rely on the capacity and scale of hyperscale data centers. Enterprises are increasingly relying on hyperscalers for hosting and also for analytics, security, and business continuity.

Sustainability and energy efficiency are also shaping the growth of the hyperscale data center industry. Operators are increasingly prioritizing renewable energy sources, advanced cooling techniques, and automation to reduce carbon footprints and operational costs. Governments and regulatory bodies are supporting these efforts with favorable policies and incentives, further fueling market expansion. Moreover, advancements in server technologies, storage solutions, and virtualization are enabling greater efficiency and higher density deployments, making hyperscale models more attractive across various industries, including finance, healthcare, and retail.

Component Insights

The hardware segment dominated the market with a revenue share of over 50.0% in 2024, driven by rising data privacy concerns and regulatory pressures that are influencing the hardware landscape as well. To ensure compliance with regional data laws and security protocols, hyperscale data centers are incorporating hardware-level encryption, secure boot processes, and advanced physical security mechanisms. These hardware innovations are crucial for maintaining data integrity and building trust among enterprise clients, thereby acting as a strong driver for continued investment and innovation in the hardware segment. The hardware segment is further bifurcated into hardware, servers, enterprise network equipment, PDU, and UPS.

The software segment is anticipated to grow at a CAGR of 15.4% during the forecast period, owing to the growing need for intelligent data center management through software-defined infrastructure. Software-defined networking (SDN), software-defined storage (SDS), and software-defined data centers (SDDC) are enabling hyperscale operators to manage resources more dynamically and cost-effectively. These technologies offer centralized control and policy-driven automation, which are critical for maintaining operational efficiency in increasingly complex infrastructures. The software segment is further bifurcated into DCIM, virtualization, and others.

Power Capacity Insights

The 50 MW to 100 MW segment dominated the market with a revenue share of over 33.0% in 2024. As hyperscale providers extend their reach into emerging markets and secondary data center hubs, they require facilities with substantial power capacities to ensure redundancy, low latency, and high availability. The 50 MW to 100 MW range allows operators to future-proof their infrastructure while accommodating regional data sovereignty laws and connectivity requirements.

The 150 MW and above segment is expected to grow at a significant CAGR over the forecast period. Hyperscale providers are increasingly consolidating their data center footprints by replacing multiple smaller facilities with fewer but larger and more efficient mega campuses. These data center parks, often built in phases, allow for long-term expansion while leveraging economies of scale in construction, operations, and energy procurement. This makes the 150 MW+ range particularly appealing for cloud giants looking to establish future-ready infrastructure capable of sustaining exponential growth for a decade or more.

Hyperscale Data Center Market Report Scope

|

Report Attribute |

Details |

|

Market size in 2025 |

USD 27.73 billion |

|

Revenue forecast in 2030 |

USD 52.54 billion |

|

Growth Rate |

CAGR of 13.6% from 2025 to 2030 |

|

Actual data |

2018 – 2024 |

|

Forecast period |

2025 – 2030 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2025 to 2030 |

|

Report enterprise size |

Revenue forecast, company share, competitive landscape, growth factors, and trends |

|

Segments covered |

Component, power capacity, enterprise size, end use, and region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; MEA |

|

Country scope |

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa |

|

Key companies profiled |

Alibaba; Amazon Web Services, Inc.; Arista Networks, Inc.; Digital Realty Trust; Equinix, Inc.; Ericsson, Inc.; Google, Inc.; IBM Cloud; Intel Corporation; Microsoft; NTT Ltd.; NVIDIA Corporation; Oracle; Rittal LLC; Tencent Cloud; Vertiv Group Corp |

|

Customization scope |

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |