Farm Implements Market growing at a CAGR of 7.1% from 2025 to 2033

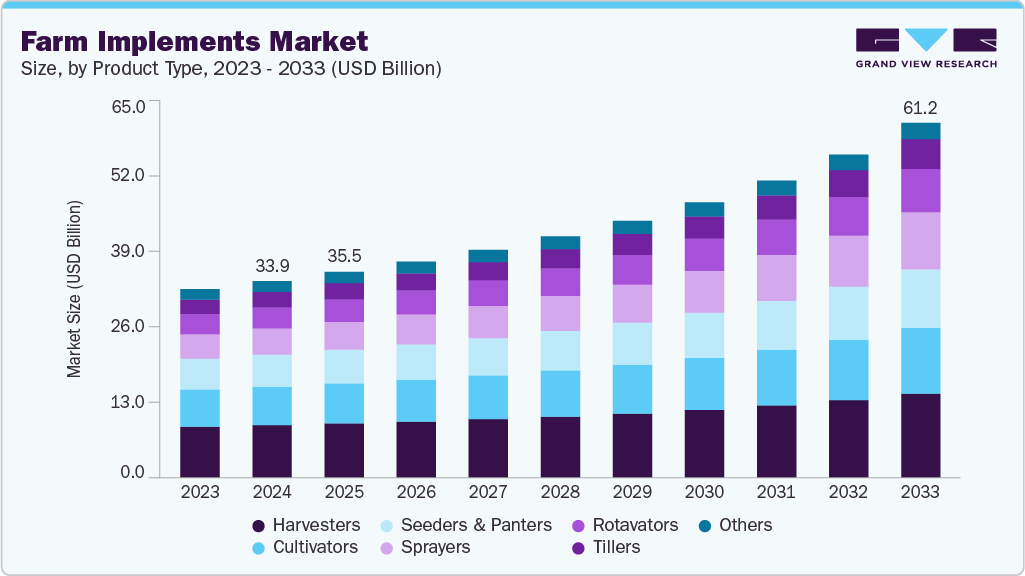

The global farm implements market size was estimated at USD 33.91 billion in 2024 and is projected to reach USD 61.18 billion by 2033, growing at a CAGR of 7.1% from 2025 to 2033. The growing focus on improving crop yield and soil health through precision and sustainable farming methods is driving demand for farm implements market

Key Market Trends & Insights

- Asia Pacific held 36.7% revenue share of the global farm implements market in 2024.

- In China, the integration of smart technologies such as IoT-enabled monitoring, and automation systems in is accelerating the demand for farm implements market.

- By security power source, management & orchestration segment held the largest revenue share of 29.6% in 2024.

- By power source, public cloud segment held the largest revenue share in 2024.

- By enterprise size, large enterprises segment held the largest revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 33.91 Billion

- 2033 Projected Market Size: USD 61.18 Billion

- CAGR (2025-2033): 7.1%

- Asia Pacific: Largest market in 2024

- Europe: Fastest growing market in 2024

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/farm-implements-market-report/request/rs1

The trend toward commercial and large-scale farming drives the farm implements market growth. As agricultural enterprises expand their cultivated areas and diversify crop types, the demand for specialized and heavy-duty equipment rises. Implements designed for high-volume operations, such as large seed drills, combine harvesters, and mechanized irrigation systems, are witnessing strong adoption. The pursuit of higher efficiency, reduced turnaround time, and scalability in farming operations is pushing both individual farmers and agribusinesses to invest in advanced implements, ensuring sustained growth of the global farm implements market.

The rapid growth of tractor sales has also had a direct positive impact on the farm implements market. Tractors serve as the primary power source for a variety of implements, including seeders, cultivators, and sprayers. As tractor penetration increases across global agricultural regions, the demand for compatible and efficient implements rises in parallel. Manufacturers are responding by developing multi-purpose and easily attachable implements that cater to diverse field conditions and cropping systems, further boosting market adoption.

The growing influence of agricultural cooperatives and contract farming models is contributing to market expansion. These models encourage collective investment in modern implements, enabling small and marginal farmers to access machinery that would otherwise be unaffordable. Cooperatives often pool financial resources to purchase high-performance equipment such as threshers, planters, or power tillers, which can be shared among members based on seasonal demand. In addition, the rise of agricultural service providers who rent out implements and machinery on a pay-per-use basis is making mechanized farming more accessible to smaller landholders, further fueling demand across both developing and developed regions.

In addition, globalization and the expansion of agricultural trade are driving the demand for advanced farm implements. As farmers aim to meet international quality standards for exports, there is a growing emphasis on uniformity, hygiene, and post-harvest efficiency. Implements that assist in precision harvesting, cleaning, grading, and packaging are becoming increasingly essential. The modernization of post-harvest operations, combined with the need to reduce crop spoilage and maintain consistent quality, is pushing the adoption of technologically sophisticated implements that streamline the entire value chain from field to market.

Product Type Insights

The harvesters segment dominated the farm implements market in 2024 with a revenue share of 26.7%. The expanding cultivation of high-value and large-scale crops such as wheat, maize, rice, and soybeans has also contributed significantly to the demand for specialized harvesters. Each of these crops requires customized harvesting solutions that ensure efficient processing and minimal crop damage. Manufacturers are responding to this demand by designing harvesters suited for specific crop types, terrains, and climatic conditions. The availability of multi-crop and modular harvesters that can handle diverse crops across seasons enhances equipment utilization rates, improving return on investment for farmers.

The sprayers segment is projected to be the fastest-growing segment from 2025 to 2033. The expansion of contract farming and custom hiring services has accelerated the use of sprayers across small and medium-sized farms. These service models enable farmers who cannot afford to own high-cost equipment to access modern spraying technologies through rental or pay-per-use systems. Agricultural input companies and cooperatives are increasingly offering mechanized spraying services as part of integrated crop management solutions. This accessibility is contributing to widespread adoption, even in developing regions. The combined effect of rising pest pressures, technological innovation, sustainability goals, and service-based farming models is ensuring strong and sustained growth of the sprayers segment within the global farm implements market.

Power Source Insights

The tractor-mounted implements segment dominated the farm implements market with a market share of over 55.3% in 2024. The growing trend toward mechanized and precision farming practices drives segment growth. Farmers are adopting tractor-mounted implements that enable more accurate and uniform field operations, improving overall productivity. Modern implements now integrate advanced technologies such as GPS, sensors, and automated depth or rate control systems, allowing for precision tillage, seeding, and fertilizer application. These innovations help reduce input wastage and optimize soil and nutrient management. The combination of tractors and precision implements enables farmers to perform multiple functions with high accuracy, thereby reducing operational time and costs. This efficiency-driven approach is particularly appealing to large and medium-scale farmers looking to maximize yield output from limited arable land.

The self-propelled implements segment is projected to be the fastest-growing segment from 2025 to 2033. The emergence of climate-resilient and adaptive farming practices is also driving the adoption of self-propelled implements. Extreme weather events, irregular rainfall, and fluctuating temperatures are affecting planting and harvesting schedules globally. Self-propelled machines provide the flexibility to operate under diverse and challenging field conditions, including wet, uneven, or hilly terrain. Their robust design and enhanced traction allow farmers to continue critical operations without significant delays, thereby mitigating the risks associated with climate variability. This reliability in unpredictable environmental conditions makes self-propelled implements particularly valuable for farmers seeking to safeguard yields and reduce losses.

Farm Implements Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2025 |

USD 35.47 billion |

|

Revenue forecast in 2033 |

USD 61.18 billion |

|

Growth rate |

CAGR of 7.1% from 2025 to 2033 |

|

Actual data |

2021 – 2024 |

|

Forecast period |

2025 – 2033 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2025 to 2033 |

|

Report coverage |

Revenue forecast, company share, competitive landscape, growth factors, and trends |

|

Segments covered |

Product type, power source, end use, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; MEA |

|

Country scope |

U.S.; Canada; Mexico UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa |

|

Key companies profiled |

AGCO Corporation; Agius Agricultural Trading Ltd.; Airtec Sprayers, Inc.; Bomet Sp. z o.o. Sp. K; CLAAS KGaA mbH; Deere & Company; Great Plains Ag; Hagie Manufacturing Company, LLC; Hiniker Company; Kinze Manufacturing; KUBOTA Corporation; KUHN Group; Landoll Company, LLC; Monosem; Remlinger Manufacturing |

|

Customization scope |

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |