Data Center Cooling Market growing at a CAGR of 22.3% from 2026 to 2033

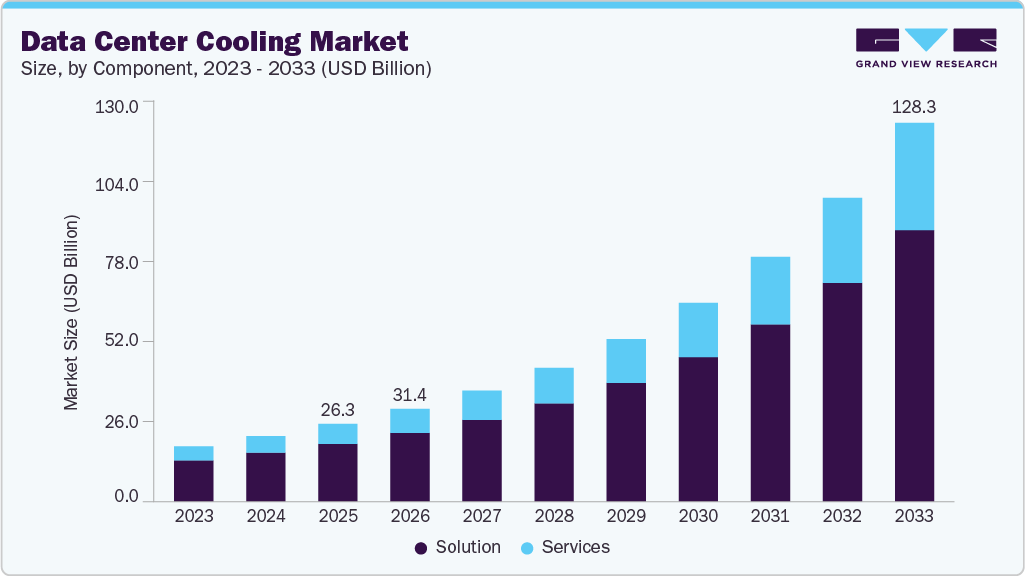

The global data center cooling market size was valued at USD 26.31 billion in 2025 and is anticipated to reach USD 128.31 billion by 2033, growing at a CAGR of 22.3% from 2026 to 2033. The growth is attributed to the rapid expansion of hyperscale and colocation data centers worldwide.

Key Market Trends & Insights

- Asia Pacific data center cooling dominated the global market with the largest revenue share of 36.9% in 2025.

- The data center cooling industry in the U.S. is expected to grow significantly over the forecast period.

- By component, the solution segment led the market and held the largest revenue share of 74.7% in 2025.

- By containment, the raised floor without containment segment led the market and held the largest revenue share in 2025.

- By application, the telecom segment is expected to expand significantly over the forecast period.

Market Size & Forecast

- 2025 Market Size: USD 26.31 Billion

- 2033 Projected Market Size: USD 128.31 Billion

- CAGR (2026-2033): 22.3%

- Asia Pacific: Largest market in 2025

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/data-center-cooling-market/request/rs1

Cloud service providers, social media platforms, and digital service enterprises continue to invest heavily in large-scale data center infrastructure to support growing data traffic and storage requirements. These facilities operate at high utilization levels and require advanced, reliable cooling systems to maintain uptime, improve energy efficiency, and comply with stringent service-level agreements.

The increasing adoption of high-density computing driven by artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), and advanced analytics workloads significantly contributes to the growth of the data center cooling industry. These applications generate significantly higher heat loads compared to traditional IT workloads, often exceeding the cooling capacity of conventional air-based systems. As a result, data center operators are increasingly investing in advanced cooling technologies such as liquid cooling, direct-to-chip cooling, rear-door heat exchangers, and immersion cooling systems to manage higher rack densities and ensure thermal stability.

A data center comprises networked computers and storage equipment for organizing, storing, processing, and disseminating data that is crucial for the functioning of a business organization. Improved network connectivity and the proliferation of smart devices are leading to an exponential increase in the volume of data generated daily. The global installed base of connected IoT devices continues to expand steadily, despite short-term macroeconomic headwinds. Total active IoT connections reached approximately 18.5 billion in 2024, representing a year-over-year increase of around 12% compared to 2023. Based on connection trends observed in the first half of 2025, the number of connected IoT devices is projected to rise by roughly 14% during the year, reaching an estimated 21.1 billion by the end of 2025.

Energy efficiency and sustainability requirements are also major contributors to market growth. Data centers are among the most energy-intensive facilities, and cooling systems account for a substantial share of total power consumption. Operators are under increasing pressure from regulators, investors, and customers to reduce carbon emissions, improve power usage effectiveness (PUE), and meet environmental, social, and governance (ESG) targets. This is accelerating the adoption of energy-efficient cooling solutions, including free cooling, evaporative cooling, adiabatic systems, and AI-driven thermal management software that optimizes cooling performance while lowering operating costs.

Component Insights

The solution segment dominated the market and accounted for the revenue share of over 74.4% in 2025. The surge in data traffic is due to the rapid increase in high-density computing workloads, particularly AI training, inference, HPC, and advanced analytics. These workloads generate significantly higher heat loads than traditional enterprise IT, rendering legacy air-based cooling architectures inefficient. As a result, data center operators are adopting integrated cooling solutions such as liquid cooling systems, rear-door heat exchangers, direct-to-chip cooling, and immersion cooling designed as end-to-end deployments rather than standalone components.

The services segment is expected to register a significant CAGR over the forecast period due to the rising complexity of modern data centers, particularly with the proliferation of high-density computing, AI workloads, and hyperscale facilities. As organizations increasingly adopt advanced cooling technologies, such as liquid cooling and modular architectures, they require specialized services to ensure optimal performance, minimize downtime, and maintain energy efficiency.

Solution Insights

The air conditioners dominated the market in 2025 due to the growth in data center densities, driven by the need for reliable and scalable thermal management in high-density computing environments. Traditional air-cooled systems remain widely deployed due to their ease of integration, lower upfront costs compared to liquid cooling, and proven operational reliability. As data centers continue to expand to support cloud services, hyperscale computing, and AI workloads, the demand for efficient air conditioning solutions that can maintain optimal server temperatures while minimizing energy consumption is increasing significantly.

The precision air conditioners segment is expected to grow at a significant CAGR over the forecast period, driven by the increasing density of IT equipment and the rising demand for high-performance computing (HPC) and AI workloads. As modern data centers deploy more powerful servers, GPUs, and storage systems, heat generation has increased substantially, necessitating the need for precise and reliable cooling solutions.

Services Insights

The installation & deployment dominated the market in 2025 due to the rising complexity of modern data centers. As organizations increasingly adopt high-density, AI-driven, and hyperscale computing environments, the deployment of advanced cooling solutions such as liquid cooling, in-row cooling, and immersive cooling systems requires specialized expertise.

The maintenance service segment is expected to grow at a significant CAGR over the forecast period. The shift toward outsourcing the management of data center operations has driven the growth of the maintenance services market. Many organizations, particularly those without in-house technical expertise, rely on specialized service providers for routine inspections, troubleshooting, and upgrades. This outsourcing trend not only drives recurring revenue for service providers but also encourages the adoption of comprehensive maintenance contracts, including performance optimization and lifecycle management.

Data Center Cooling Market Report Scope

|

Report Attribute |

Details |

|

Market size in 2026 |

USD 31.39 billion |

|

Revenue forecast in 2033 |

USD 128.31 billion |

|

Growth rate |

CAGR of 22.3% from 2026 to 2033 |

|

Actual data |

2021 – 2025 |

|

Forecast period |

2026 – 2033 |

|

Quantitative units |

Revenue in USD million/billion, and CAGR from 2026 to 2033 |

|

Report services |

Revenue forecast, company share, competitive landscape, growth factors, and trends |

|

Segments covered |

Component, solution, services, type, containment, structure, application, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa |

|

Key companies profiled |

ABB; Air Enterprises; Asetek, Inc.; Climaveneta ClimateTechnologies PVT. LTD.; Coolcentric. Dell Inc.; Fujitsu; Hitachi, Ltd.; Johnson Controls; Mitsubishi Electric Corporation; Nortek Air Solutions, LLC; NTT Ltd.; Rittal GmBH & Co. KG.; Schneider Electric; STULZ GMBH; Vertiv Group Corp |

|

Customization scope |

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |