Dispersing Agents Market growing at a CAGR of 5.8% from 2026 to 2033

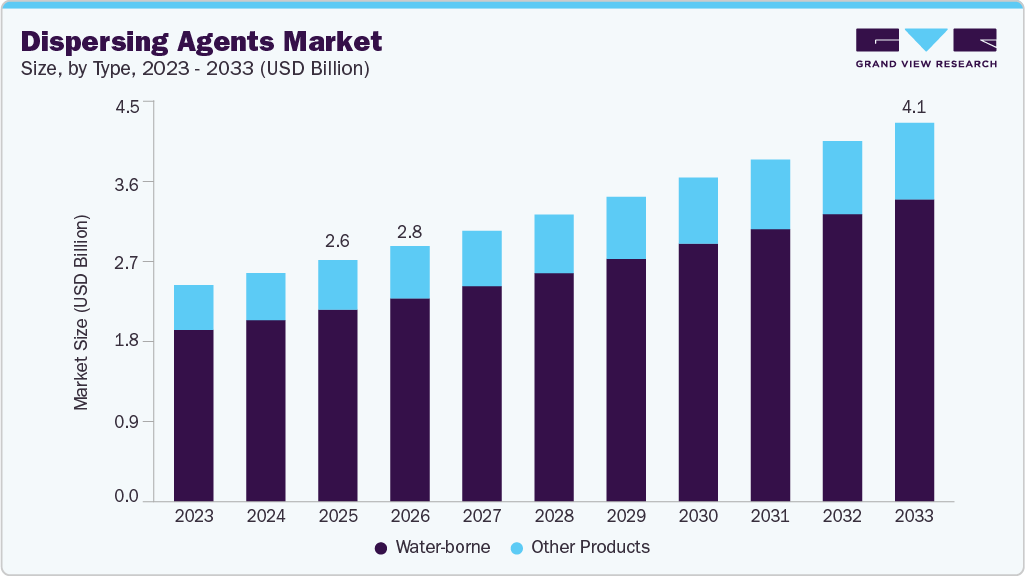

The global dispersing agents market size was estimated at USD 2,598.5 million in 2025 and is projected to reach USD 4,077.3 million by 2033, growing at a CAGR of 5.8% from 2026 to 2033. This growth is attributed to the rising application of dispersing agents in the paints, coatings, and inks industry, coupled with increasing construction activities across the globe.

Key Market Trends & Insights

- Europe dominated the global dispersing agents market with the largest revenue share of 51.2% in 2025.

- The dispersing agents market in Germany led Europe in 2025.

- By product, the water-borne segment held the largest revenue share of 79.5% in 2025.

- By structure, the anionic segment led the market, accounting for the largest revenue share of 38.4% in 2025.

- By end-use, the paints, coatings, and inks segment held a dominant position in the market, accounting for the largest revenue share of 39.0% in 2025.

Market Size & Forecast

- 2025 Market Size: USD 2,598.5 Million

- 2033 Projected Market Size: USD 4,077.3 Million

- CAGR (2026-2033): 5.8%

- Europe: Largest market in 2025

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/dispersing-agent-market/request/rs1

Dispersing agents play a critical role in the paints and coatings industry by enhancing the performance and stability of the final product. These agents help prevent pigment agglomeration or settling, ensuring uniform dispersion and consistent color quality.

The construction industry continues to witness significant growth, supported by increased infrastructure development, urbanization, and renovation activities worldwide. Dispersing agents play an essential role in construction materials such as paints, coatings, adhesives, and sealants by improving the dispersion of pigments and solid particles, thereby enhancing performance, durability, and aesthetic properties. In addition, ongoing technological advancements in construction materials are leading to the development of high-performance formulations that require efficient dispersion of additives and fillers, which is expected to drive market demand over the forecast period.

The market is further supported by rising demand from both established and emerging end-use industries, including oil and gas, paper, paints and coatings, detergents, pharmaceuticals, agriculture, automotive, and others. The increasing adoption of dispersing agents across these sectors reflects the growing need for improved material dispersion, stability, and formulation efficiency in complex industrial processes.

The automotive industry represents a key end-use segment contributing to market growth. According to the International Trade Administration, the U.S. remains one of the largest automotive markets globally and ranks second in vehicle production and sales. Rising automotive production and refinishing activities are expected to support demand for dispersing agents over the forecast period, as these additives play a critical role in achieving uniform dispersion of pigments, fillers, and other components in automotive coatings, ensuring consistent color, enhanced durability, and improved performance.

Market Concentration & Characteristics

The global dispersing agents market is moderately fragmented, characterized by the presence of multinational chemical companies alongside regional specialty additive manufacturers. These players benefit from established distribution networks, strong relationships with end-use industries, and diversified product portfolios catering to coatings, construction, plastics, and agrochemical applications. Key participants are increasingly focusing on capacity expansions, investments in advanced formulation technologies, and development of high-performance and sustainable dispersing solutions to strengthen their competitive positioning in the global dispersing agents market.

Leading players in the global dispersing agents market are adopting a combination of capacity expansion, product innovation, strategic collaborations, and sustainability-driven initiatives to strengthen their market presence. Companies active across specialty chemicals, additives, and formulation solutions are investing in advanced dispersion technologies, performance-enhancing chemistries, and next-generation dispersing agents to improve stability, compatibility, and efficiency across end-use applications. To address rising demand across Asia Pacific and Central and South America, several market participants are expanding manufacturing capabilities, strengthening regional distribution networks, and collaborating closely with formulators and end-use industries to support localized supply needs and application-specific performance requirements.

Product Insights

The water-borne segment dominated the market, accounting for the largest revenue share of 79.5% in 2025. This dominance is attributed to the growing demand for sustainable and environmentally friendly products across industries such as paints, coatings, and inks. Water-borne dispersing agents support the development of eco-friendly formulations, as they are typically surfactants or polymeric compounds with hydrophilic properties that enable interaction with water molecules. These agents contain functional groups capable of adsorbing onto particle surfaces, reducing interfacial tension between particles and the liquid medium. As a result, particles are more easily dispersed and effectively prevented from agglomeration or settling.

Other dispersing agent types, including solvent-borne and oil-borne variants, are expected to grow at a CAGR of 5.6% over the forecast period. Solvent-borne dispersing agents are designed to disperse solid particles in solvent-based systems and are composed of organic compounds with high solubility in the formulation solvent, thereby improving performance and enhancing the durability of the final product. Oil-borne dispersing agents, on the other hand, are specifically formulated for oil-based systems and are widely used to disperse pigments and solid particles in oil-based paints, varnishes, and coatings.

Structure Insights

The anionic segment led the market, accounting for the largest revenue share of 38.4% in 2025. This dominance is attributed to the wide range of applications of anionic dispersing agents across paints, coatings, inks, adhesives, and ceramics. These agents offer excellent dispersion stability by preventing particle agglomeration or settling, resulting in improved color development, reduced viscosity, and enhanced overall performance of the final product. Furthermore, anionic dispersing agents are particularly well-suited for water-based systems, which are increasingly preferred due to tightening environmental regulations and growing health and safety concerns. Their effectiveness in dispersing pigments and additives in water-based coatings, inks, and related formulations continues to support strong demand.

The non-ionic segment is expected to grow at a CAGR of 5.9% over the forecast period, driven by broad compatibility with various charged molecules and relatively low toxicity. These characteristics make non-ionic dispersing agents suitable for diverse applications, including textiles, pharmaceuticals, and personal care products. In addition, their ability to stabilize emulsions under extreme conditions and enhance dispersion efficiency in paints, coatings, and inks contributes to increasing adoption. The ongoing shift toward eco-friendly and bio-based formulations, along with regulatory pressures favoring sustainable chemical solutions, is further accelerating demand for non-ionic dispersing agents.

The amphoteric segment is also expected to witness notable growth during the forecast period. Amphoteric dispersing agents possess both hydrophilic and hydrophobic properties, enabling them to interact effectively with both water-based and non-polar systems. Unlike purely hydrophilic or hydrophobic dispersants, amphoteric agents contain functional groups that can ionize under both acidic and alkaline conditions, typically derived from amino acid-based structures such as glycine or betaine. This dual-charged nature allows them to interact with a wide range of particles regardless of surface charge.

Dispersing Agents Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2026 |

USD 2,749.5 million |

|

Revenue forecast in 2033 |

USD 4,077.3 million |

|

Growth rate |

CAGR of 5.8% from 2026 to 2033 |

|

Base year for estimation |

2025 |

|

Historical data |

2018 – 2024 |

|

Forecast period |

2026 – 2033 |

|

Quantitative units |

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Product, structure, end-use, region |

|

Regional scope |

North America; Europe; Central and South America |

|

Country scope |

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Brazil; Argentina; |

|

Key companies profiled |

BASF SE; Arkema; Kemira; Solvay S.A.; Altana AG; Dow; Evonik Industries AG; Clariant; Uniqchem; Rudolf GmbH; The Lubrizol Corporation; Italmatch CSP; Nouryon; SNF |

|

Customization scope |

Free report customization (equivalent to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |