Green Propellants growing at a CAGR of 12.2% from 2025 to 2033

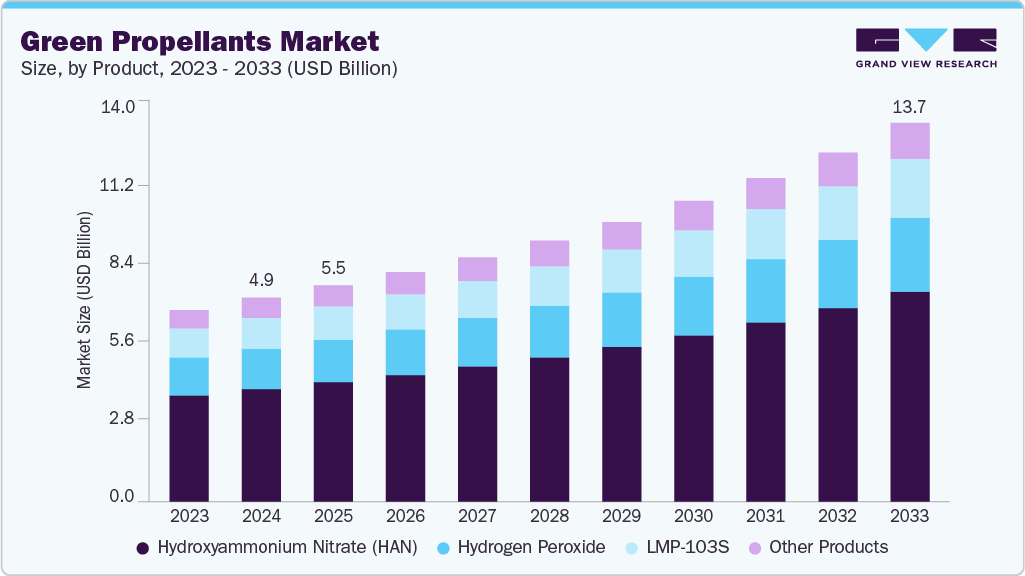

The global green propellants market size was estimated at USD 4.96 billion in 2024 and is projected to reach USD 13.72 billion by 2033, growing at a CAGR of 12.2% from 2025 to 2033. The green propellants are used specifically in rockets.

Key Market Trends & Insights

- North America dominated the global green propellants market with the largest revenue share of 39.9% in 2024.

- The green propellants market in the U.S. accounted for the largest market revenue share in North America in 2024.

- By product, the hydrogen peroxide segment led the market with the largest revenue share of 34.1% in 2024.

- By application, the satellites segment is expected to grow at the fastest CAGR of 12.3% from 2025 to 2033.

Market Size & Forecast

- 2024 Market Size: USD 4.96 Billion

- 2033 Projected Market Size: USD 13.72 Billion

- CAGR (2025-2033): 12.2%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/green-propellants-market-report/request/rs1

The market is driven by increasing regulatory and safety pressure to replace toxic, legacy hypergolic propellants (e.g., hydrazine-based fuels). Governments, space agencies and commercial operators increasingly prioritize crew and ground-station safety, lower handling and disposal costs, and stricter environmental controls, all of which favor low-toxicity, less volatile alternatives.

A second major driver is mission performance and lifecycle economics. Modern green propellants deliver comparable or improved specific impulse, storability, and thermal stability for many in-space maneuvers (attitude control, station-keeping, orbital transfer) while reducing the cost and complexity of ground support, fueling infrastructure, and PPE. When the total cost of ownership is modeled, including handling, transportation, environmental remediation, and mission risk, green propellants increasingly show attractive payback for small-sat constellations, geostationary satellites, and in-orbit servicing vehicles, encouraging broader commercial adoption.

Governments, space agencies, and commercial operators increasingly prioritize crew and ground-station safety, lower handling and disposal costs, and stricter environmental controls, all of which favor low-toxicity, less volatile alternatives. These regulatory and institutional shifts shorten procurement lead times for demonstrator and operational programs that commit to green propellants. This creates near-term demand from agencies and prime contractors seeking lower compliance risk and insurance exposure.

The accelerating commercialization of space and the rise of small satellites, rideshare launches and distributed constellations are expanding the addressable market for green propellants. Commercial satellite operators prefer solutions that simplify launch integration, reduce hazardous-material restrictions at launch sites, and enable rapid turnaround between missions. Coupled with active R&D, successful flight demonstrations, and growing supplier ecosystems (propellant manufacturers, thruster makers, fuel handling equipment), these market dynamics are driving rapid technology maturation and scaling, which in turn feed further adoption across government and private space programs

Market Concentration & Characteristics

The green propellant industry is defined by a small set of technically differentiated chemistries (e.g., HAN-based monopropellants, LMP-103S, concentrated H₂O₂) that trade higher specific impulse and density against easier handling, lower toxicity and reduced ground-support costs compared with legacy hydrazine systems. These propellants are supplied both as fuels and as integrated thruster systems (HPGP/LMP-103S, HAN monopropellant thrusters) and are evaluated for compatibility with existing feed systems, materials and thermal architectures, a key technical gating factor for adoption.

Flight demonstrations and agency assessments have validated performance and handling benefits (reduced PPE and range constraints) while highlighting mission-integration considerations (pre-heat needs, materials compatibility) that buyers weigh during procurement.From a market standpoint, green propellants sit in an early-commercial / scaling phase: uptake is driven by regulatory and safety pressures to replace toxic hypergols, the economics of lifecycle handling and launch-site constraints, and expanding demand from small-sat constellations, in-orbit servicing and some defense uses. Suppliers range from specialist propellant manufacturers and thruster OEMs to systems integrators; value is realized not only in fuel sales but in thruster hardware, loading services and ground-support simplification.

Green Propellants Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2025 |

USD 5.46 billion |

|

Revenue forecast in 2033 |

USD 13.72 billion |

|

Growth rate |

CAGR of 12.2% from 2025 to 2033 |

|

Base year for estimation |

2024 |

|

Historical data |

2021 – 2023 |

|

Forecast period |

2025 – 2033 |

|

Quantitative units |

Volume in kilotons, Revenue in USD million/billion, and CAGR from 2025 to 2033 |

|

Report coverage |

Revenue forecast, volume forecast, competitive landscape, growth factors, and trends |

|

Segments covered |

Product, application, end use, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; Saudi Arabia; South Africa |

|

Key companies profiled |

Bellatrix Aerospace; Mitsubishi Heavy Industries; Aerojet Rocketdyne; Ariane Group; ISRO; NASA; Deutsches Zentrum Fur Luft-und Raumfahrt (DLR); L3Harris Technolgies; Ball Aerospace |

|

Customization scope |

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |