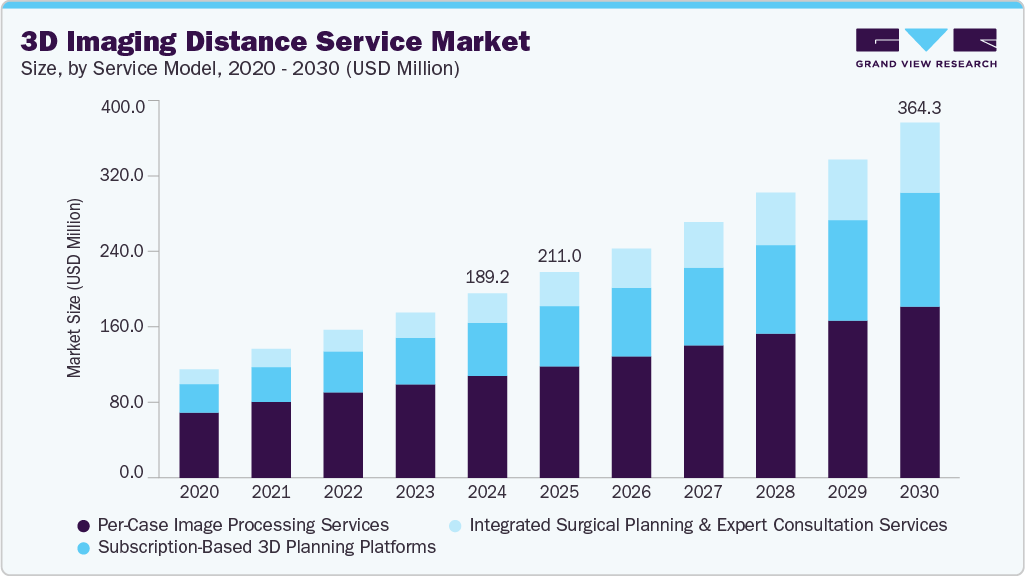

3D Imaging Distance Service Market growing at a CAGR of 11.5% from 2025 to 2030

The global 3D imaging distance service market size was estimated at USD 189.2 million in 2024 and is projected to reach USD 364.3 million by 2030, growing at a CAGR of 11.5% from 2025 to 2030. The growth is driven by rising demand for improved diagnostic precision, minimally invasive procedures, and telehealth integration.

Key Market Trends & Insights

- North America 3D imaging distance service market dominated the global industry and accounted for a 54.3% revenue share in 2024.

- By service model, the per-case segment led the market with a 55.3% share in 2024.

- By application, the general surgery segment led the market with a 32.5% share in 2024.

- By sales method, direct sales to hospitals/clinics segment accounted for the largest market share at 46.9% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 189.2 Million

- 2030 Projected Market Size: USD 364.3 Million

- CAGR (2025-2030): 11.5%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/3d-imaging-distance-service-market-report/request/rs1

Advanced imaging technologies enable real-time collaboration, preoperative planning, and medical education. In 2025, the U.S. is projected to report approximately 2.04 million new cancer cases and 618,120 cancer-related deaths, with lung, colorectal, and pancreatic cancers being the leading causes of mortality.

The industry is expanding as healthcare providers increasingly utilize advanced imaging to refine surgical planning, particularly for high-risk cancers. The demand for personalized and minimally invasive procedures fuels the use of 3D technologies that improve tumor targeting and reduce surgical trauma. Surgeons now rely more on 3D models for tailored interventions, especially in complex fields like colorectal and gynecologic oncology. Innovations in AI-driven 3D imaging and real-time visualization are revolutionizing surgery by enhancing outcomes, minimizing complications, and improving efficiency. Endometrial (or uterine) cancer-currently the sixth most common cancer in women globally-poses a growing clinical burden.

Market Concentration & Characteristics

The industry is moderately concentrated, with a mix of established imaging firms and emerging tech startups driving innovation. Key players focus on cloud-based platforms, AI integration, and telehealth compatibility to meet the rising demand for remote diagnostics and surgical planning.

The industry is characterized by rapid technological advancements, increasing applications in oncology and complex surgeries, and growing emphasis on personalized, minimally invasive care. Strategic collaborations with healthcare providers and regulatory support for digital health solutions shape market dynamics. Precision-focused 3D imaging services are becoming essential for improving clinical outcomes and operational efficiency as value-based care gains traction.

The industry is characterized by high innovation, driven by rapid tech advancements and rising clinical needs. MeVis Medical Solutions, a Varex Imaging subsidiary, highlighted innovations at RSNA 2023, including AI-powered Veolity LungCAD and LungRead for lung nodule detection and CT scan analysis. Their MeVis Distant Services (MDS) suite enables 3D visualizations from CT/MRI data for surgical planning in liver, kidney, and pancreas procedures. It also supports vascular analysis and secure remote collaboration through shared 3D models. The MeVis Liver Suite enhances hepatobiliary surgical planning, combining detailed imaging with user-friendly tools for clinical teams.

The industry is significantly shaped by evolving regulatory frameworks to ensure patient safety, data security, and clinical efficacy. Regulatory bodies like the FDA, EMA, and regional health authorities mandate rigorous compliance for software-as-a-medical-device (SaMD) solutions. Data protection laws such as HIPAA and GDPR further influence how patient imaging data is stored, transmitted, and shared, especially across borders. Certification standards for AI integration and interoperability with hospital information systems also affect product development and deployment timelines. Adherence to these regulations ensures quality and trust, but present hurdles that require substantial investment in compliance infrastructure.

Mergers and acquisitions influence the industry, reshaping competitive dynamics. A key example is KARL STORZ’s January 2024 acquisition of Innersight Labs Ltd., a UK-based AI innovator known for its Innersight3D software. This platform converts CT and MRI scans into interactive, web-accessible 3D models tailored to patients. The acquisition strengthens KARL STORZ’s offerings by integrating AI-enhanced 3D imaging tools, enabling more precise preoperative planning, shorter surgeries, and fewer complications. Such strategic moves highlight how companies leverage M&A to boost innovation, expand capabilities, and respond to growing demand for advanced surgical visualization technologies.

Product substitutes in the industry include traditional 2D imaging techniques, in-person diagnostic imaging services, and standard radiology consultations. While these alternatives may offer lower costs or easier access in some regions, they lack the precision, depth, and real-time collaboration features provided by 3D imaging. Emerging technologies like augmented reality and virtual reality-based visualization tools pose substitution threats but often serve complementary roles. However, the growing demand for minimally invasive procedures, personalized care, and remote diagnostics continues to strengthen the position of 3D imaging services, limiting the appeal of substitutes and reinforcing their value in clinical workflows.

3D Imaging Distance Service Market Report Scope

|

Report Attribute |

Details |

|

Market size value in 2025 |

USD 211.0 million |

|

Revenue forecast in 2030 |

USD 364.3 million |

|

Growth rate |

CAGR of 11.5% from 2025 to 2030 |

|

Actual data |

2018 – 2024 |

|

Forecast period |

2025 – 2030 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2025 to 2030 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Service model, application, sales method, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; MEA |

|

Country scope |

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; Thailand; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait. |

|

Key companies profiled |

Medannot; Ceevra, Inc.; Visible Patient (VP); EDDA Technology, Inc.; Materialise NV; MeVis Medical Solutions AG; 3D Systems, Inc.; Innersight Labs Ltd.; Precision Image Analysis, Inc.; 3DR Labs, LLC. |

|

Customization scope |

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail customized purchase options to meet your exact research needs. Explore purchase options |